Did Economic Reforms Unleashed in 90/91 succeed? Part I.

Did Economic Reforms Unleashed in 90/91 succeed?

Thirty years, after introducing Economic Reforms [ER-91] in 90/91, we continue to debate if they worked, and if so how well. Now that they are being reversed in some very fundamental ways under Modi, it becomes all the more necessary to understand what prompted ER-91, what were their key objectives, and how they succeeded or failed. Unless we understand that, assessing the merits of the changes now being pushed on the economy by Modi under the garb of ERs will be impossible.

What prompted ER-91?

The reforms were triggered by insolvency of the external sector of the economy, where we had run a persistently adverse trade balance since independence, and made up the difference by borrowing abroad. In the 80s, we ran up very large current account deficits, and financed these through sovereign borrowings disguised as commercial borrowings of the public sector, who actually had no need for such funds. Nor was it easy to recycle their huge cash balances created by external borrowings through the economy.

In effect, Govt borrowed abroad to balance the books but without being able to use the money productively for investments. The result was predictable. The economy sank after an initial euphoria fueled by borrowings, creating no export earnings to repay loans, and bankruptcy threatened. So the first and foremost aim of ER-91 was to stave off bankruptcy.

How was this done? Firstly, throwing previous inhibitions to the wind, foreigners were allowed to buy certain classes of assets in India, especially equity of private corporate sector, but also some PSUs. As we shall see, this was the most successful part of reforms that staved off bankruptcy, allowing us to pretend to be solvent again, by selling the family silver to foreigners.

From the chart above you can see FDI, as percentage of GDP has grown from practically nil in 1990 to high of 4% of GDP in 2005. It has fallen off from that peak to a steady flow of 2% of GDP.

To achieve a 10% growth rate, at an ICOR of 5, India needs a savings rate of 50% of GDP of which only 30% obtains today. We need another 20% in savings from either the domestic sector, or from FDI. So the the 2% FDI we get today is a pittance compared to our need for growth. The FDI does help the BOP situation, but is clearly far less than what is required to step up growth from around 6% today to the desired 10% level.

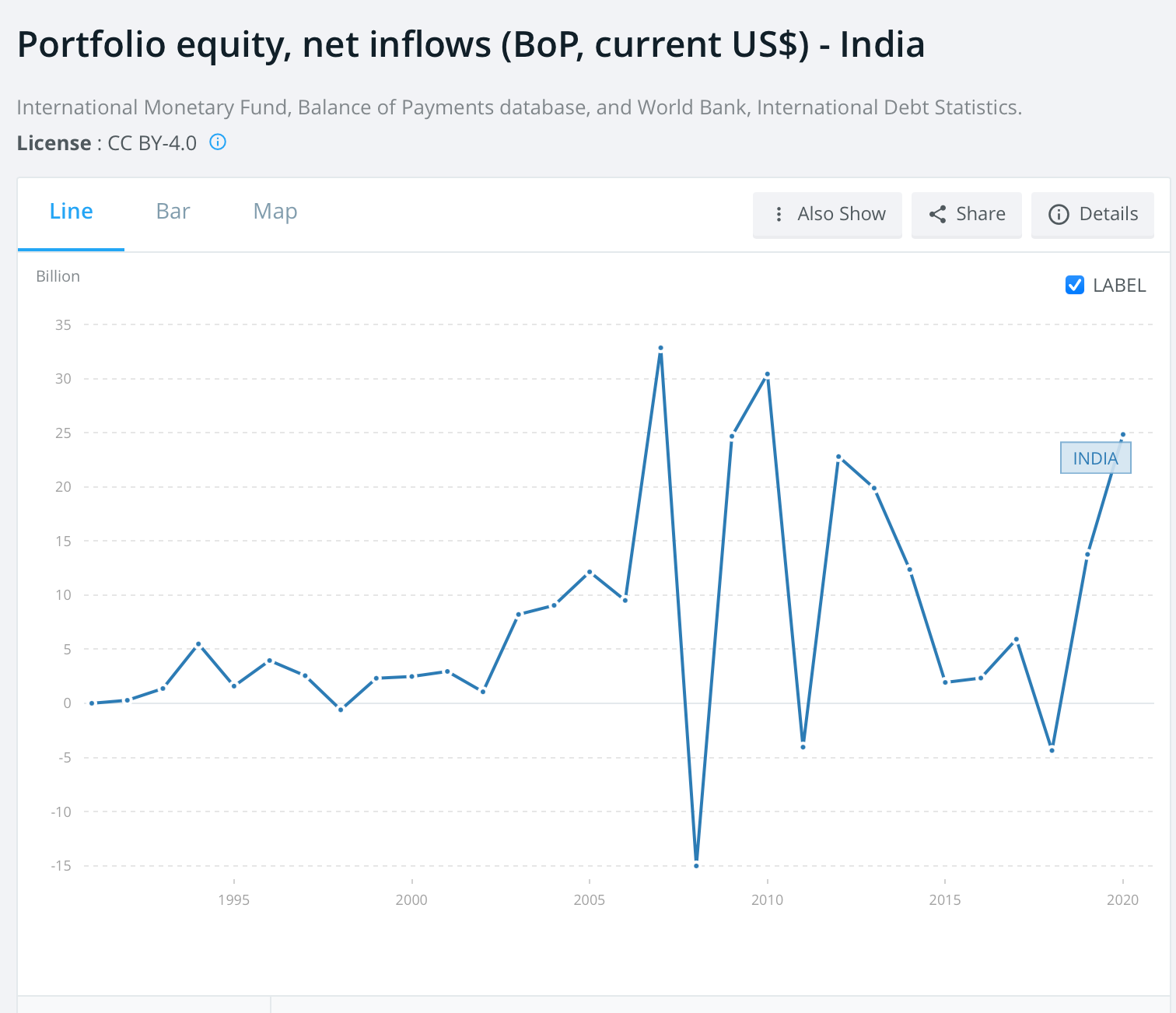

FPI are another source of savings in the economy. They are not as reliable as FDI because they include a large speculative element, and they also reverse pretty often. Roughly, FPI flows add about $20 billion to the pool of domestic savings. I don’t reckon them as over above the 2% FDI because they are already a part of the overall domestic savings of 30% or so. Nevertheless, they help address the current account balance deficit.

In principle, there is nothing wrong in selling some equity in Indian enterprises to foreigners. This sucks in foreign investment, increases domestic corporate access to capital markets abroad, and adds to the pool of domestic savings, making a larger quantum of investments possible.

That is the theory. It holds good provided you use the cashflow thus generated, to address the structural component of the adverse trade balance, and correct the Current Account Deficit [CAD]. Has that happened? The answer is mixed.

The CAD moderated for some years, helped largely by export earnings from software services, which in turn benefitted from the devaluation of the INR against the Dollar as part of the reforms package. But the CAD never disappeared. And is still with us. We continue to live beyond our means as before.

Meanwhile, as we continued to sell the family silver to live beyond our means, we have now come to stage where the supply of family silver has been nearly exhausted. In some blue chips like HDFC Bank, foreigners now hold 74% of the equity. There are sharp limits to the extent to which you can sell your vital assets to foreigners while pretending to “own” them.

The pernicious effect of this artificial solvency has erased from our minds the stark fact that FPI flows have to repaid; that all told, they are a more expensive form of borrowing than debt - both for corporates and the economy - and that mere accounting rules don’t change the nature of such borrowings.

As in the 1980s, we are living in an artificial bubble of prosperity created by borrowings abroad: In the 1980s it was via public sector borrowings, pretending that they weren’t sovereign borrowings; now it is via FPI flows, and pretending that these are non-repayable equity, instead of borrowed funds in the form of equity.

Clever economists will point out that in a bankruptcy, the repayment value of such equities will be zero. True. But let not said clever economist forget that for this to happen, we ourselves, and the economy, will have to go zero first. This clever argument is bogus.

So what’s the read on success or failure of the reforms judging from the objective of making the economy stand on its feet, and making the polity live within it means?

Well, the reforms bought us 30 years of more growth, and that is welcome.

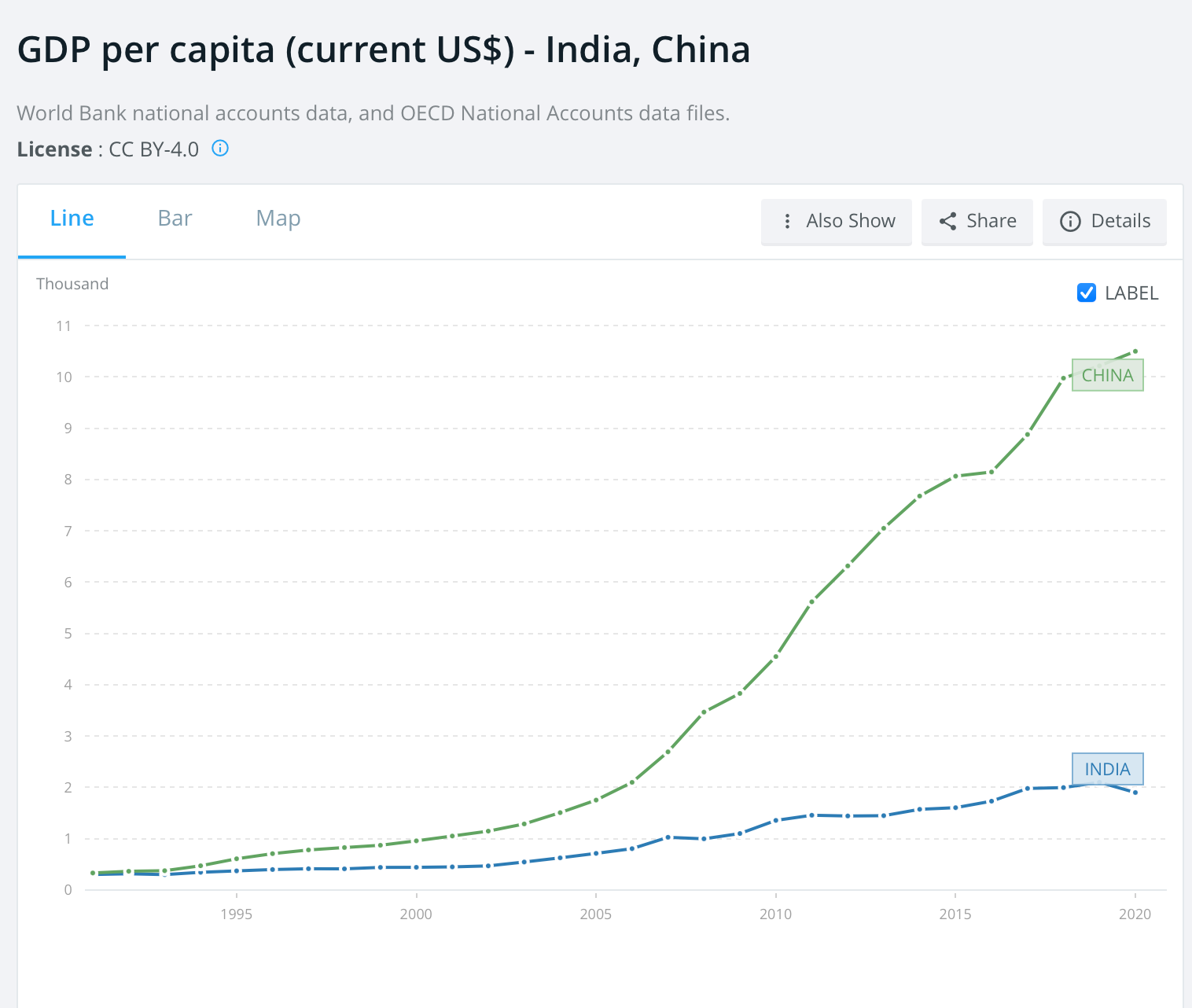

But meanwhile we made no changes in the economy that would enable more exports, and reduce dependence on imports, on an enduring basis. Nor did we augment the pool of domestic savings to permit higher investment for the future without borrowing abroad. So while, per capita GDP in India grew from $303 in 1991 to a high of $2100 in 2019, in current Dollars, ie 7X times, the same in China grew from $330 in 1991 to a high of 10,500 in 2019, that is 32X times.

Note two things about the above graphs. China and India started from more or less the same spot in 1991 with per capital GDP at $300. The per capita GDP from China began is huge surge beyond India in 1995-2000, especially after our nuclear tests, and never looked back. Those nuclear tests in retrospect cost us a lot, as we shall see.

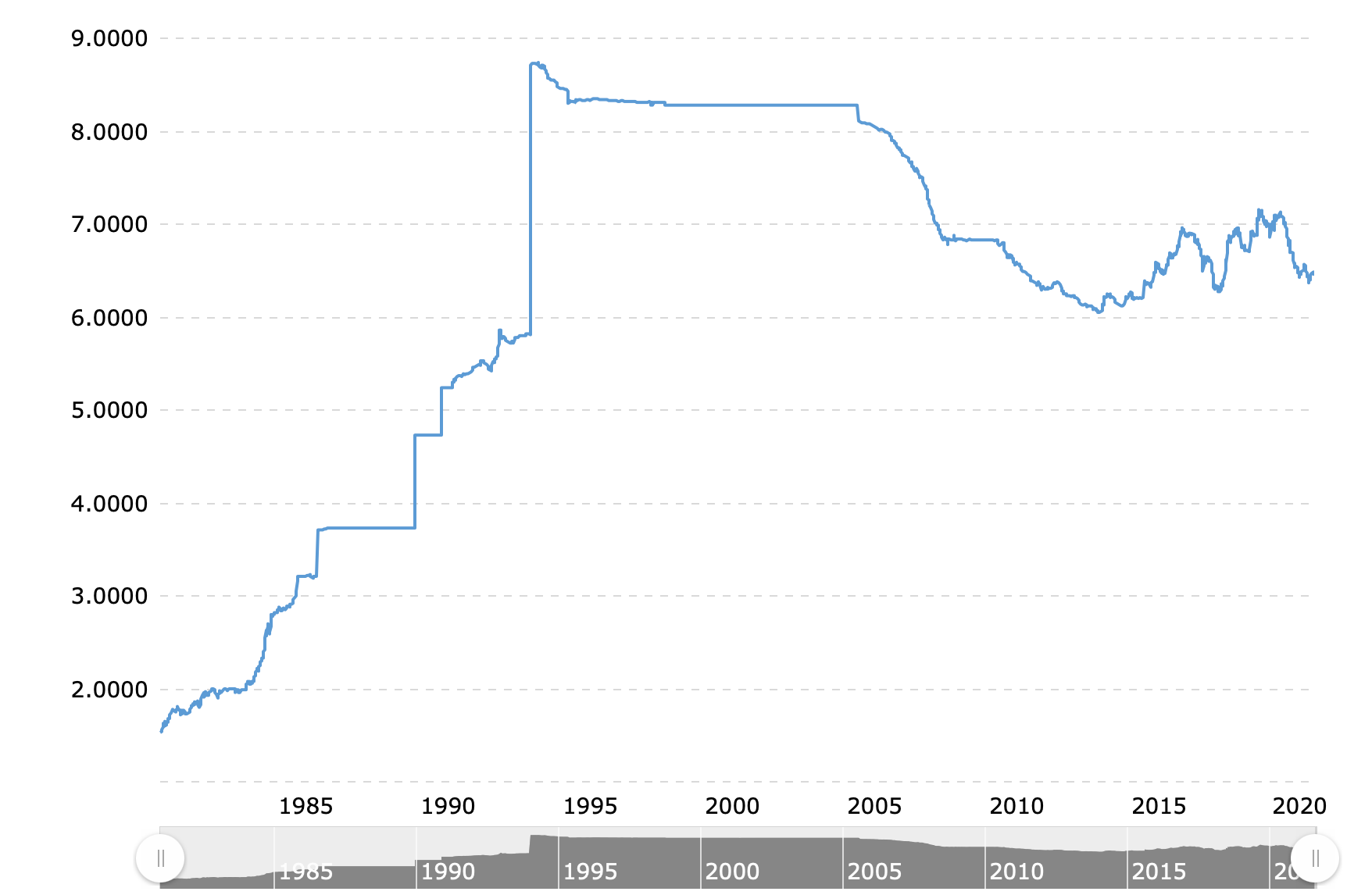

Secondly, China devalued the Yuan from Y3.700 to the Dollar, to Y9. 000 to the Dollar between 1990 and 1993, and thereafter closely pegged the Yuan to the Dollar. This devaluation actually began from 1.5 Yuan to the Dollar in 1981. Notice how steeply China had to drop the external value of the Yuan [ by a factor of 6X] in order to suck out manufacturing activity from the US to its factories. Do take time and contrast this with the Dollar-INR rate during the same period. How in the world could our manufacturing compete with China given this scenario? Yet, to the best of my knowledge such comparisons are never brought to light by our economists. It is as if they exist only to shoot India in the head and foot.

The chart is below:

Note the effect this had on FDI in China, in contrast to what happened in India.

As we can see “the starting conditions” make all the difference to the “race.” In my previous essay Understanding labor arbitrage I had explained how a devaluation of your currency exposes the hidden value of the non-trade-able portion of your economy for outside investors to use, either through FDI or by buying your exports.

What China did was steeply drop the external value of its Yuan by a factor of 6X outbidding India by a wide margin for FDI from the US when investors from there were seeking to shift manufacturing to cheaper location. In one fell stroke China wiped India off the high table and while we were congratulating ourselves at having staved of bankruptcy. Such the folly and lack of depth of understanding amongst our policy makers. This failure to view trade as a completive business, rather than just trudge along “managing the economy” lies at the heart of our failure to keep up with China.

Ironically, since the FDI assets never go away, and the assets of the non-trade-able portion of your economy remain where they are - at home - the temporary drop in value of these through a steep devaluation is more like a limited time period “discount window” to attract buyers. Soon after you devalue, as investments catch up, the value of your non-trade-able economic assets is restored by markets and your currency catches up. [Though China carefully pegged Yuan to the Dollar for a decade to ensure that new investments had time to yield results before allowing market to assert itself.] The result can be seen from charts. FDI in China soared to 6% of GDP, and settled down at about 4% of GDP. But during the critical ten years 1990-2000, China left the value of its domestic assets at 50% of India values, and walked away with most of the manufacturing in the US, while we were celebrating our nukes.

The problem is, not having diagnosed why we lost out, we are now repeating the same old mistakes under Modi by doubling down on bad, inward oriented policies that favor rent seeking tycoons rather than dynamic exporters.

Nor did we honestly tell ourselves that our swelling mountain of foreign reserves were actually borrowed riches, and a drain on our domestic savings pool. We preferred the false illusion of prosperity, great power status, and dreams of sitting on the global high table. Did the world believe us? Alas the world is not as dumb as us.

There were two very adverse fall-outs from an inadequate understanding of reforms.

Firstly, the Dutch Disease. This is a debilitating malady caused by allowing borrowings abroad [debt + FPI] to inflate the external value of the INR, such that it inhibits exports and encourages dependence on imports. The REER vs NEER charts clearly point to the pernicious effect of the Dutch disease on our CAD.

The way NEER vs REER has been managed would make a fit case for treason against the Indian economy. In the following essay I will show, using US and China productivity data, and labor participation rates to demonstrate how deeply flawed RBI model for adjusting REER for relative productivity changes between India and our main trading partners - US and China are.

For now I will leave with a synopsis of the data. Technical issues of Substack prevent doing all this in one post.

Briefly, RBI calculations of productivity [relative to that of our main competitors, US and China] in its models do not consider the Labour participation rates at all. The result is like saying those without jobs don’t matter at all to the economy. The fact is if a farmer produces X units of GDP, and but that leaves one person unemployed, then the GDP per person is X/2 and not X. But more on this later.

That 30 years of above par GDP growth have not enabled us to eliminate the structural component in our CAD, and the fact the growth in exports has fallen as a percentage of GDP since 2005, are ample proof of the Dutch disease.

[More proof of this when I deal with REER vs NEER in the following essay.]

The second baneful effect of the creeping Dutch disease was duty inversion across several critical industries especially electronics and computers.

If you keep letting the value of INR creep up relative to the Dollar, for sustained periods of time, the imported cost of the finished good, say a TV set, becomes cheaper relative to the imported cost of the components, and value added to them locally, which is in INR, making imports of TV sets cheaper than local manufacture.

When smart traders see this happening in India, they carefully target such vulnerable local manufacturers, driving them out of business with a combination of predatory pricing, and carefully selected market segments. As a result, whole swathes of Indian consumer electronics, and computer hardware manufacturers, were driven out of business via Chinese imports.

Later, the same thing was repeated in pharmaceutical APIs. But in all those years, while this was happening, policy makers did not give a hearing to complaints from manufacturers, nor make the needed policy adjustments in time. Belated adjustments in exchange rates were made only when a crisis struck - usually long after the manufacturer had gone under, diminishing industry, and destroying jobs. The story repeats itself under Modi in a slightly different guise but with the same baneful effects on local manufacturing and jobs.

It should therefore come as no surprise that industry loathed the Congress Govt. and its pusillanimity in pushing the full suite of reforms. Nor is their switch of allegiance to Modi any surprise. He has promptly addressed their need by raising tariff walls, and duty protection.

However, please note, the economy’s consumers pay the bills in both cases, and are the net losers. Congress pusillanimity hurt them by destroying local jobs and reducing incomes, while Modi makes them foot the bill via higher imported prices. Both ways the economy is hurt. And our competitors are better off than before. Congress tone deafness to duty inversion was legendary. Modi’s remedy makes the malady worse.

This essay continues to part II to discuss, the success, or lack of it, of the ER-91 package. In particular, Part II discusses how China knocked us off from the Asian high table, using exchange rates as strategy, relative productivity of the two economies, and the reduction in poverty in India made possible by the step up in the alpha growth rate of GDP from 4% prior to reforms, to 7% thereafter.

The whole idea was less governance via phasing out License Raj. Post MAY 2014 general elections its CRONY RAJ via the Blackhole called Electoral bonds. But even NO Guarantees as TATA found to their chagrin.

Fascinating to read. These two essays must find its way into some textbook where they teach policy making. That data about mfg. vis-a-vis services, and the shabbily treated Services industry is quite stunning. Great to read!